Let me add some additional commentary.

The crux of the issue @nope seems to have is that our protocol fees are too high. So let’s think about this from first principles.

First, basically all DEXs have protocol fees, certainly all major ones on Solana. Prior to dynamic fees, Lifinity had a fixed protocol fee of 15%. Apparently this was acceptable because no one complained.

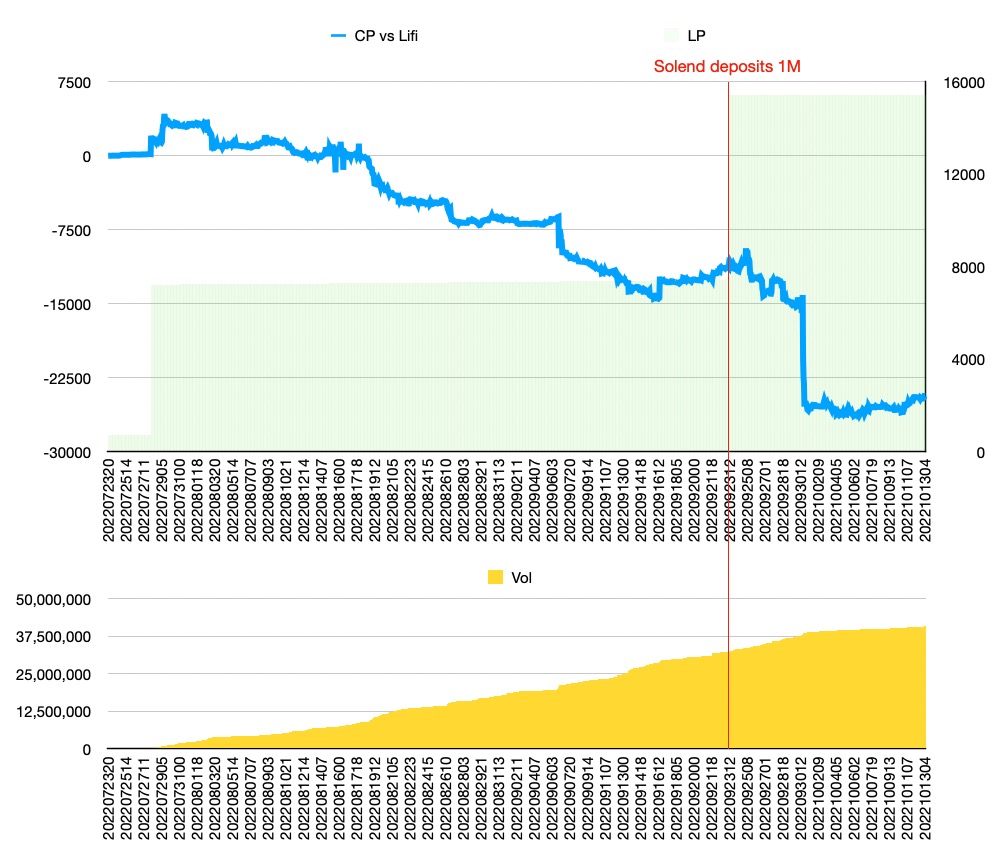

Once we switched to dynamic fees, the fee for the mSOL-USDC pool became 100% because it had more liquidity than the target liquidity. Now Solend starts to complain. (And let’s be clear, it’s just Solend because they are basically the only other LP in the pool besides Lifinity.)

So the natural conclusion, then, is that there is some value between 15% and 100% past which a larger protocol fee becomes unacceptable, for whatever reason. We know that this value isn’t 15%, because there are DEXs on Solana that have a MNDE gauge and also have a protocol fee higher than 15%. So where is the threshold? Is it 20%? 30%? 50%? 99%?

The answer to this question is subjective. There is no “correct” answer. Any choice is purely arbitrary.

So then, who should decide? Apparently, @nope believes that they or the Marinade community should be able to determine what is “too high” or “too low”, what the magical threshold is where DEXs aren’t disincentivizing deposits too much (newsflash: any and all protocol fees disincentivize deposits). This is nonsense.

In July, Solend introduced interest rate spread fees, which disincentivizes deposits compared to before (lower deposit APR). Should I push for Marinade to remove Solend’s gauge because they don’t incentivize deposits as much as they used to? Of course not. A protocol’s fee structure should be decided by the protocol itself, not by Marinade. It is a self-regulating mechanism because if a fee structure is bad no one will deposit, which will then incentivize the protocol to improve it. Or if deposits are not useful beyond a certain point (which is the case for Lifinity) and the protocol runs optimally at the current level of deposits or less, there is no need to incentivize additional deposits.

Suppose Lifinity were to lower its protocol fee. The only difference would be that Solend receives more trading fees. It would not increase Marinade TVL nor change the level of liquidity provided. So at bottom, this discussion is about whether Solend “deserves” more trading fees. It doesn’t concern Marinade governance.

The MNDE rewards for Lifinity’s mSOL-USDC pool still fulfill their purpose of attracting more liquidity to the pool. It’s not as if Lifinity is blocking those rewards from LPs. It’s also not as if dynamic fees cause there to be less liquidity than the originally promised $1M.

If people don’t like that the gauges incentivize a fixed amount of liquidity on Lifinity, perhaps they should suggest ideas for how to improve how the gauges work rather than merely try to shut down a single gauge.