Abstract

With the successful rollout of the Stake Auction Marketplace (SAM), Marinade has introduced a powerful new mechanism that allows validators to bid for stake, guarantee APY, and drive yields beyond the market standard.

Distributing almost 9M in SOL stake across the network, Marinade’s SAM was able to achieve an auction-winning APY of 11.41%, significantly higher than the market average, with 149 out of 405 validators currently securing bids through SAM.

Combined with the Protocol Staking Rewards (PSR), which protected over 2,500 SOL from validators’ downtime, it’s clear that Marinade’s innovations are driving tangible value and resilience in the Solana staking ecosystem.

Building on this momentum, the DAO recently passed MIP.5 on MetaDAO, which introduced MNDE-Enhanced Staking. At the core of that proposal was introducing a fee share of 10% from the SAM Performance Fees to MNDE stakers, introducing tangible utility to MNDE for the first time since Directed Stake was phased out to make way for SAM.

To further amplify the value proposition for MNDE holders and compound the benefits of MIP.5, we now propose an additional upgrade: redirecting 40% of the performance fees currently streaming to the Treasury toward buying back the MNDE token.

Accordingly, this proposal would delegate the decision of “whether to direct 40% of the SAM performance fees to MNDE buybacks” to a decision market created by MetaDAO. The market will determine whether this change should be expected to impact the Marinade Finance ecosystem positively.

If adopted, this proposal would authorize Marinade DAO to take the following actions, conditional on the decision market accepting the proposal:

- Extend the bid system to direct 40% of SAM performance fees to buy back the MNDE.

- Grant authority of this system and its various parameters to Marinade DAO

Motivation

This proposal will seek to achieve the following key effects:

- Buying back undervalued MNDE tokens and putting them on the DAO’s balance sheet.

- Further aligning incentives for non-validator MNDE holders apart from earning a portion of the performance fees (pursuant to MIP.5).

- Introducing sustained buy pressure and added utility for MNDE alongside MNDE-Enhanced Staking.

Decision markets enable us to measure whether a proposal passing would truly affect the value of the Marinade protocol.

Key Terms

APY: Annual percentage yield (APY) is a figure that represents the actual amount of interest earned on investments and savings.

Auction Winning Set Of Validators: Validators that have the highest bids and meet all additional requirements for the delegation strategy.

Decision Market: Conditional markets stipulate that if and only if this were to happen, your trade would be realized. The counterfactual is valid as well.

Delegation Strategy: The strategy Marinade uses to direct SOL towards validators. This includes the SAM as well as MNDE-Enhanced Staking.

Futarchy: A market-driven decision-making governance system. Fut — future, archy — governance. MetaDAO has created a platform for trading these markets.

Liquid Staking: Enable people to stake without losing access to the liquidity of their tokens through tokenization and issuance of on-chain representations of staked assets — liquid staking tokens — that are a claim on the underlying staked positions.

MNDE Buybacks: A mechanism through which SAM performance fees are used to purchase MNDE tokens from the open market. These tokens are then moved to the DAO treasury, reducing circulating supply, introducing buy pressure, and aligning incentives across stakers and token holders.

mSOL: mSOL is a liquid staking token that you receive when you stake SOL on the Marinade protocol. These mSOL tokens represent your staked SOL tokens in Marinade’s stake pool.

MNDE: Marinade’s governance token.

Protected Staking Rewards (PSR): The bond for the validator used to ensure the max yield is delivered.

Stake Auction Marketplace (SAM): The Stake Auction Marketplace allows Marinade stakers to delegate SOL to validators offering the best APY.

Specifications

Before the rollout of SAM several months ago, the MNDE token commanded significantly more control over the protocol, directing a substantial stake deposited in Marinade to validators of their choice. SAM, however, unified the stake distribution process, allowing 100% of Marinade’s TVL to be distributed through SAM. While this resulted in a significantly better UX for validators — and a higher APY for Marinade Liquid and Native stakers alike — MNDE holders’ utility was significantly diminished.

MIP.5 — which will take effect soon — was a step in the right direction, re-introducing tangible utility to MNDE holders by allowing them to capture a portion of performance fees generated by the protocol.

However, as seen below, the projections for MNDE-Enhanced Staking, while impressive (estimating an implied 10% APR on the low end), didn’t represent a complete overhaul of the MNDE tokenomics / value flows.

| mSOL TVL | ~$1.6B | Est. Return |

|---|---|---|

| Aggregate Projected Yield | 9.5% | $152M / yr |

| DAO Performance Fee | 9.5% | $14.4M / yr |

| MNDE-Enhanced Staking Reward | 10% (95 bps) | $1.4M / yr |

| MNDE Staked | 100M ($14M) | |

| Est. Participation Rate | 10 - 20% | |

| Est. Return to MNDE-Staked | $1.4M - $2.8M | $1 - $2 / per dollar MNDE |

Accordingly, by introducing a token buyback — akin to JUP, RAY, and MPLX — the Marinade DAO is able to induce a virtuous flywheel wherein MNDE supply is gradually reduced (taken off the market), subsequently placing direct buy pressure on the MNDE and increasing staking yields (as fewer tokens chase rewards), and so on.

Apart from acting as a complementary mechanism to MNDE-Enhanced Staking and placing direct buy pressure on the MNDE token, these buybacks also serve as a way to:

- Bolster the Marinade DAO Treasury by acquiring potentially undervalued MNDE tokens and placing them on the DAO’s balance sheet.

- Encourage liquidity provisioning for the MNDE token, as buybacks are shared equally across all MNDE sinks — stakers, LPs, etc. alike, unlike performance fee sharing, which can only be borne by MNDE stakers.

With the introduction of these buybacks along with MNDE-Enhanced Staking, the MNDE token will now have a meaningful way to directly participate in the upside of the Marinade protocol through exposure to performance fees both via staking rewards and buybacks. Increasing the capped amount of SOL that can be staked with a given validator in the winning set of validators — MNDE-Enhanced Stake Cap — along with token voting (governance) on RealmsDAO will remain ancillary mechanisms and utilities for the MNDE token.

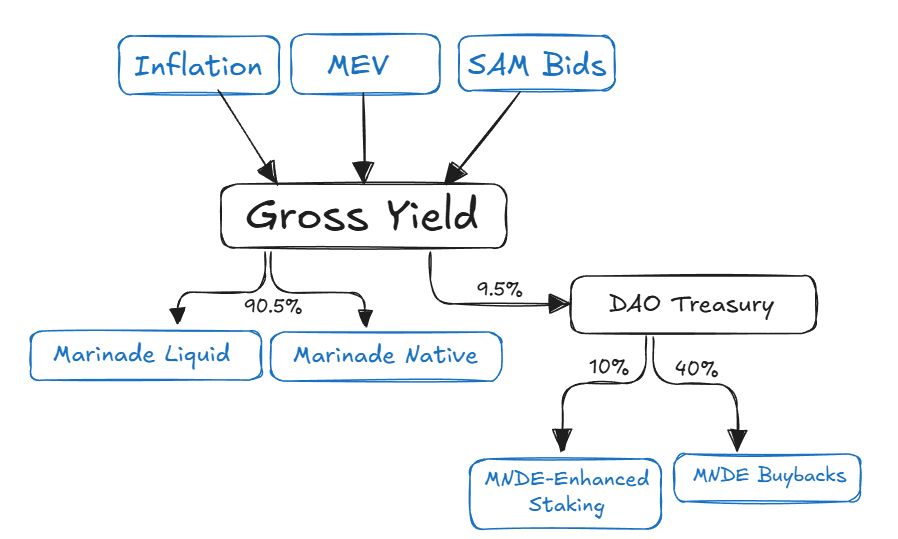

Put together, of the 9.5% performance fee taken from the SAM gross yield, 50% would remain in the treasury, 10% would go to MNDE-Enhanced Staking, and 40% to on-chain MNDE buybacks, as seen above. Specifically, 40% of the previous month’s performance fees would be used to acquire (buy back) MNDE strategically, with reports being published in the month after the buybacks to inform the community on execution and other pertinent details.

Projected Performance

| Marinade Finance TVL | ~$1.2B | Est. Return |

|---|---|---|

| Projected Gross Yield | 9.5% | $114M / yr |

| DAO Performance Fee | 9.5% | $10.83M / yr |

| MNDE Buybacks | 40% | ~$4.33M / yr |

Currently, with a market capitalization of $36.5 million, we can estimate — heuristically — that the DAO is on track to buy back roughly 12% of MNDE’s market cap per year — a significant source of protocol-driven buy pressure for the MNDE token.

Futarchy parameters

The decision market will be initialized with a description containing a link to this proposal and the memo text: “If approved, this proposal would sanction the development and implementation of MNDE buybacks according to the specifications laid out in MIP.11.”

- The pairing of the decision market will be MNDE-USDC.

- MetaDAO will initialize the market with $10,000 in USDC and an equivalent value of MNDE. It will be left to the discretion during proposal creation to increase the liquidity as required.

- The pass threshold will be set to 3%, meaning that the proposal will pass if, and only if, the time-weighted average price in the pass market is 3% or more greater than the time-weighted average price in the fail market.

- The market will run for 3 days in slot time, which means that if Solana experiences downtime during the proposal, that downtime will not affect the amount of time traders have to participate in the decision market.

- For the TWAP parameters, the first observation will be set to the spot price of MNDE tokens on the date of market creation, as determined by CoinGecko, and the max observation change per minute will be set to $0.001. In practice, this means that if someone is able to manipulate the price for an hour without being detected, they would move the observation by approximately 40% and the total TWAP by approximately 0.33%.

Benefits / Risks

Benefits

- Increased utility and buy pressure for the MNDE token.

- Less discrimination for MNDE LPs as the benefits of buybacks are absorbed by all.

Risks

- Acquiring overvalued MNDE / selling undervalued SOL tokens as the buyback strategy — at least initially — will not have any regard for current prices (by virtue of their temporal nature).

- Price impact / slippage when buying back MNDE tokens.

Outcomes

- Update the value flows of the protocol to direct 40% of the performance fees to MNDE buybacks.

- Realms update and management of these parameters.

The governance process is unique here, with the role of MetaDAO’s market in the decision.

Step 1: 5-day discussion period of this proposal on the forum

Step 2: 5-day voting period on realms, including the 2-day cool down period

Step 3: If MIP.11 passes, the MetaDAO market will determine whether the proposal meets the established criteria

Step 4: Implementation. This could require additional Realms configuration and votes if programmatic changes are required.

The decision posed to the Marinade DAO in MIP.11 is not whether to support this implementation. The vote is to authorize a MetaDAO market on this proposal and honor the outcome if the MetaDAO market exceeds the passing threshold. If the MetaDAO market fails, any further action would be subject to full DAO approval.

Cost Summary

This proposal will reallocate 40% of performance fees — which is 9.5% of the SAM staking yield — from the treasury to buy back the MNDE token on the open market.